As we approach the end of 2023, we can start to asses the performance over the past 12 months (11 from time of writing) of the various asset classes both traditional and alternative, and go further to look at the performance of the various securities that operate within said asset classes. This article will consider the commodity sector and separate the star performers from the poor performers.

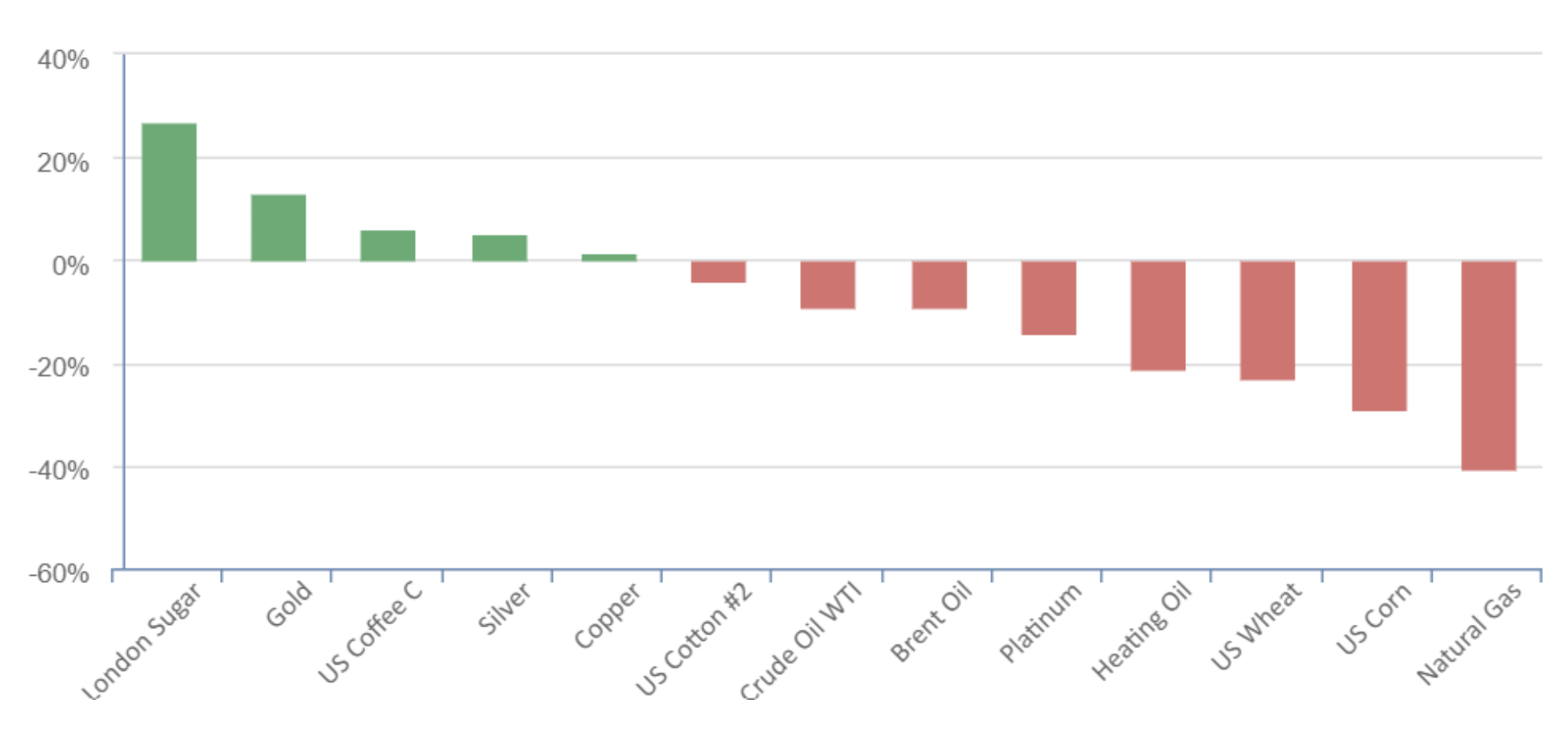

Gold has increased by more than 13% in 2023

Last week was a significant one in the commodity sector as gold hit $2,150 per troy ounce for the first time, taking its 2023 gain to over 13%. Golds impressive performance has come from a variety of factors:

- Softer economic data combined with less hawkish signals from the Fed has injected optimism into markets that the Fed might be done raising interest rates.

- Gold is a safe-haven asset, and with the tensions in the middle east now potentially rising after a US warship and other vessels were attacked in the Red sea, this impact risk sentiment.

- The dollar has weakened in recent months, the gold and dollar often exhibit an inverse relationship, investors now have to spend more dollars to buy gold.

Gold is not the only metal to perform well this year, silver has gained roughly 4.5% this year, with a very noticeable gain of 11% in November.

Oil down 9% in the energy sector towards year-end

Not all commodity sectors have performed well, oil has struggled. Crude Oil WTI is down almost 9% this year, natural gas has plummeted 40%, and Brent oil is down 9%.

The struggles were exacerbated last week after the much awaited OPEC meeting disappointed. OPEC is responsible for 40% of the world’s oil supply, and markets were up pre meeting on the expectation of more aggressive cuts in supply. The meeting disappointed markets with the outcome being further voluntary cuts led by Russia and Saudi Arabia.

Figure 1 – Commodities YTD performance, Investing.com

What global economic outlook can we expect in 2024?

As we start to look ahead to 2024, we continue to ask ourselves the same questions. Will the Fed really drop borrowing costs less than 6 months into the year? Will the US enter a recession and if so how bad will it be? Will the increasing tensions in the middle east be manageable or will there be further conflict? There are some of the key questions of which the answers will have a sizeable effect on financial markets.

Unfortunately no one has a crystal ball, but what we do have is history, and there is nothing new under the sun. If conflicts were to increase it is likely that we’ll see the price of gold rise, along side oil if the supply chain is affected. This is likely to be the case if other major oil players are drawn into the conflict.

If the US were to enter a recession, (which is likely as indicated by the inverted yield curve on gov bonds) we would likely see this having a negative impact on stocks. This year markets have been propelled by the “magnificent 7” (Tesla, Apple, Meta, Microsoft, Nvidia, Alphabet, and Netflix) who now make up 30% of the S&P 500, if you remove those stocks the index has achieved a much more humble 6% this year. Disappointing Q4 results for the big 7 could be a telling start to the year.